Signs of the Economic Apocalypse, 6-26-06

Gold closed at 586.00 dollars an ounce on Friday, up 0.2% from $584.70 the Friday before. The dollar closed at 0.7996 euros Friday, up 1.1% from 0.7910 for the week. The euro closed at 1.2507 dollars compared to 1.2640 at the end of the week before. Gold in euros would be 463.61 euros an ounce, up 0.2% from 462.47 at the previous Friday’s close. Oil closed at 70.84 dollars a barrel on Friday, up 1.2% from $69.97 for the week. Oil in euros would be 56.64 euros a barrel, up 2.3% from 55.34 at the end of the week before. The gold/oil ratio closed at 8.27, down 1.1% from 8.36 for the week. In the U.S. stock market, the Dow Jones Industrial Average closed at 10,989.09, down 0.2% from 11,014.55 for the week. The NASDAQ closed at 2,121.47 on Friday, down 0.4% from 2,129.95 at the close of the previous week. The yield on the ten-year U.S. Treasury note closed at 5.22%, up 9 basis points from 5.13 for the week (and up 25 basis points over the last two weeks).

Not a lot of change in the markets last week with the exception of long term interest rates in the United States (the ten-year Treasury up 25 basis points in two weeks). The widespread use of risky adjustable rate mortgages in the United States makes such interest rate increases potentially catastrophic:

Rising interest rates and foreclosures, in turn, lead to lower prices and sharp slowdown in the overall housing industry (including financial services workers, construction and renovation skilled tradespeople, real-estate agents, bankers and lawyers, hardware and home improvement retailers and those who manufacture all those goods sold by Ace and Home Depot and the lumber stores. All that now comprises a good chunk of the U.S. middle class.Foreclosures may jump as ARMs reset

By J.W. Elphinstone, AP Business Writer

As more hybrid adjustable rate mortgages adjust upward and housing prices dip, many Americans can't refinance out of this squeeze. They are finding themselves trapped in too-high monthly payments, and some face foreclosures.

In 2003, Anita Britten refinanced her two-story brick cottage in Lithonia, Ga. using a hybrid adjustable rate mortgage, or ARM. Her lender reassured her that she could refinance out of the riskier loan into a traditional one when her interest rate started to reset.

Three years later, Britten can't get a new mortgage and her monthly payment has jumped by a third in six months. She can't afford her payments and may face foreclosure if her financial situation doesn't change.

For those who can't make their payments, foreclosure is the only way out.Foreclosure figures just released by the Mortgage Bankers Association show that foreclosure activity fell in the first quarter of 2006 over the first quarter of 2005 for all loan categories except subprime loans. The MBA didn't specify how many of subprime loans were adjustable rate mortgages.

In the last several years, millions of Americans took equity out of their houses and refinanced when interest rates were at historical lows and housing prices were at record highs.

Many of them chose to refinance into hybrid ARMs that lenders were aggressively pushing. ARMs, which featured a low introductory interest rate that resets upward after a set period of time, were easier to qualify for than traditional fixed-rate loans.

…This year, more than $300 billion worth of hybrid ARMs will readjust for the first time. That number will jump to approximately $1 trillion in 2007, according to the MBA. Monthly payments will leap too, many beyond what homeowners can afford.

For example, Britten's monthly payment jumped from $1,079 to $1,340 at the beginning of this year. It rose again on June 1 by another $104 and is scheduled to increase again in December. Britten, who is also paying off student loans, went to a credit counseling service to help her avoid foreclosure.

"I've gotten rid of all my credit cards and I'm not supposed to refinance for another year," she said. "All I can do is tread water right now."

"ARMs are a ticking time bomb," said Brad Geisen, president and chief executive of property tracker Foreclosure.com. "Through 2006 and 2007, I'm pretty sure we'll see a high volume of foreclosures."

Last year, foreclosures hit a historical low nationwide at about 50,000. But that number has more than doubled since then, according to Foreclosure.com.

And delinquency rates appear to be rising, as well. While delinquency rates fell for most types of loans from the fourth quarter of 2005 because of a stronger economy, delinquencies for both prime and subprime ARM loans increased year-over-year in the first quarter, according to the MBA.

The hardest hit states so far are those that have experienced the roughest times economically. Michigan, Texas and Georgia lead the pack, specifically around Detroit, Dallas and Atlanta, whose major employers have run into strikes, bankruptcies and industry downturns.

But as the housing market slows, experts expect foreclosures to skyrocket in those areas that have experienced the highest appreciation rate — like California, Florida, Virginia and Washington, D.C.

"There is a direct correlation between foreclosure sales and market activity," said Dr. James Gaines, a research economist at The Real Estate Center at Texas A&M University. "If the rate of appreciation is not there, then there is an increase in foreclosure sales."

Gaines pointed out that although California's default notices are rising by the thousands, actual foreclosure sales remain in the hundreds. Because of California's still-active housing market, homeowners there can sell their properties before going into foreclosure.

On the flip side, in less active markets like Texas and Georgia, homeowners can't find a buyer in time and are forced into foreclosure.

But as the housing cools in these once hot markets at the same time that ARMs reset, many homeowners may be unable to dump their properties before going into foreclosure, Gaines predicts.

Additionally, Gaines pointed out that these same real estate markets also boasted a higher percentage of ARM originations, because most buyers could only get into their homes using an unconventional loan.

California, where the median home price reached $468,000 in April, leads the nation in the percentage of homes purchased with adjustable rate mortgages. Nationwide, ARMs account for 24 percent of all home loans.

"In our zeal to make mortgage lending more available to a greater number of people, it's normal to expect the foreclosure rate to go up," Gaines said.

Even investors in foreclosures are having a harder time finding good deals, as the housing market cools. Many homes that do end up in foreclosure auctions are saddled with more than one mortgage and have little or no equity — so the investors take a pass.

Falling home values are also affecting homeowners' ability to refinance into a traditional 30-year fixed rate loan to avoid foreclosure.

In 2002, Christopher Jones, 32, refinanced into a hybrid ARM with plans to refinance again when the rate started to readjust. At the time, his downtown Atlanta house appraised for $108,000.

Now, his monthly payments have shot up, but Jones can't sell his house for more than $84,000 and he can't get an appraisal for more than $85,000.

The appraisal firm told Jones that the value of houses in his neighborhood have fallen victim to a cooling market. With no other options left, Jones has decided to pack it in and foreclose on the house.

"I'm just going to take the loss," he said. "That's all I can do."

Some homebuyers, especially first-time buyers, may not have fully understood the risk of ARMs. In the rush to close on a house sale, especially in the frenzied market of the past few years, many first-time buyers often failed to get the full details of their loan from their mortgage broker.

"Sometimes buyers are very optimistic of how much mortgage they can handle, especially in a strong housing market with aggressive marketing of riskier mortgages," said Suzanne Boas, president of Consumer Credit Counseling Services of Greater Atlanta.

When Dora Angel of DeSoto, Texas bought her first home in 2003, she paid $141,000 for the brand new three-bedroom, two-bath home. At the time, her mortgage payment was $1,400 a month.

DeSoto originally thought that she had a fixed-rate loan. But about five months ago, she noticed that her monthly payment kicked up to $1,900. She only made the monthly payments by sacrificing payments on her credit cards, which pulled down her credit rating.

Now, DeSoto can't continue paying $1,900 each month, but, because of her credit ranking, she doesn't qualify for a fixed-rate mortgage.

"I was a first-time buyer. I was blind. I didn't know what questions to ask," she said. "And the mortgage brokers are there telling you what you want to hear just to get you in the mortgage."

Unfortunately, during a runaway market, many buyers, sellers and mortgage brokers were more excited about making deals than making smart deals, and the fallout has just begun.

"We are on the front of this ARM problem. It will roll out over the next several years," Boas said. "Owning a home is the American dream, but losing one is the ultimate nightmare."

Home sellers, builders feel pinch of slowdownBut enough about the United States. What about the rest of the world? Well, nowadays, it’s all tied together:

By Andrea Hopkins

Thu Jun 22, 12:34 PM ET

When Keith Gersin saw the perfect four-bedroom house in southern Ohio four years ago, he jumped to buy it before anyone else could snap it up. When he finally sold it last month, it went for $30,000 less than he had hoped -- and that after seven months on the market.

In retrospect, the 41-year-old physician admits he overestimated the U.S. housing market, which has begun cooling after five years of record-breaking sales and double-digit price appreciation.

"I was naive," said Gersin, who sold his Cincinnati-area home in May to move to North Carolina with his wife and son. He made about $60,000 on the sale, but had hoped for better.

"Everyone thinks their house is the most beautiful in the world, so it comes as a bit of a shock when it doesn't sell right away."

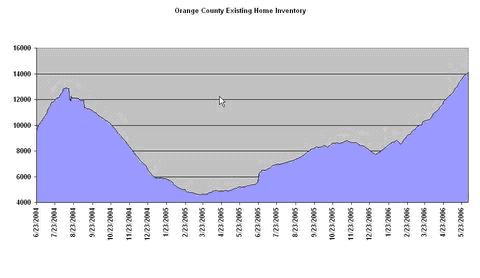

The housing slowdown -- sharp in some regions and more gradual in others -- is seen by many economists as an inevitable and even healthy moderation to an overheated market. Even so, for many homeowners, real-estate agents and builders, the market's new direction is not particularly welcome.

With mortgage rates rising, sales of existing homes were 5.7 percent slower in April than they were a year earlier, and the inventory of new homes is at a record high.

The rising supply of unsold homes makes it that much harder for homeowners to get the sale price they hoped for.

"In our neighborhood, on our street, there were three houses that went up for sale within months of each other," said Gersin.

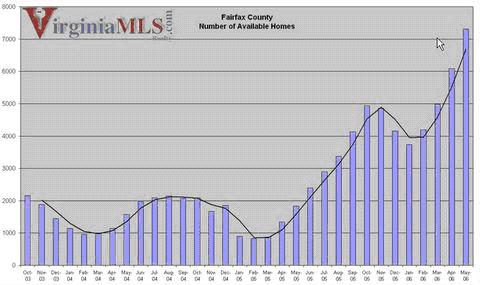

Cincinnati real-estate agent Jeff Schnedl has seen a shift in the market.

"It is absolutely slower. Some areas are still chugging along but even those are chugging along more slowly than they used to," said Schnedl, who has been selling homes in the Ohio River city for five years.

A drive down any street in Cincinnati, whose suburbs straddle Ohio, Kentucky and Indiana, turns up plenty of "For Sale" signs -- with the occasional "Price Reduced" addendum slapped on top.

Schnedl said homes are staying on the market longer.

"There is a lot more inventory on the market this year than last year -- about 25 percent more. So buyers have more homes to choose from and that slows the sale cycle down. Plus with rising interest rates, people are thinking harder. That slows it down, too."

The average rate on a 30-year fixed mortgage rose to 6.63 percent last week, up a full percentage point from 5.63 percent last year, according to mortgage finance company Freddie Mac.

Such an increase boosts the cost of a $200,000 mortgage by about 11 percent, or $129 a month, to $1,281 -- an unwelcome jump for consumers who are already feeling the pinch of soaring energy prices.

The housing slowdown is also being felt by home builders. While housing starts rose 5 percent in May, permits for future groundbreaking -- an indication of builder confidence -- dropped to the lowest level since 2003, government figures showed this week…

A hard landing in 2006 – just not in the US?

Brad Setser

Jun 18, 2006

Nouriel and I postulated back in early 2005 that there was a meaningful risk that the next “emerging market” crisis might come from the US – and it might come sooner than most expected. The basic quite simple: Ferguson’s debtlodocus might find that it no longer could place its debt with the world’s central banks, the dollar would fall, market interest rates would rise, US debt servicing costs would go up, the economy would slow and the value of a host of financial assets would tumble.

Why the emphasis on central banks? Simple: they have been the lender of last resort for the US, financing the US when private markets don’t want to. See April 2006. Consequently, a truly bad scenario for the US seemed to require a change in central banks’ policies. Real emerging markets aren’t so lucky. When private markets don’t want to finance them, they typically aren’t bailed by someone else’s central bank.

It sure doesn't look like sudden stops in financial flows and sharp markets moves have been banished from the international financial system. Certainly not this year. They just didn't strike the US, but other countries with large and rising current account deficits.

Iceland’s currency is way down (its stock market too) even though interest rates on Icelandic krona are up. The private market’s appetite for krona disappeared.

Inflation is up too, driven by the weak krona.

The Turkish lira is way down. Lira interest rates are way up – as is Turkish inflation.

Turkey's central bank sold dollars this week -- for the first time in quite some time. It was buying dollars in a big way in the first quarter. Times change.

Currency collapses do not necessarily translate into economic slumps. That was a key point that the Federal Reserve has made in response to fears about a US hard landing. A fall in the currency doesn’t always translate into higher interest rates, at least in post-industrial countries. And in part because lots of the damage from a fall in the currency comes when firms, banks and the government have borrowed in foreign currency, turning a currency crisis into a debt crisis.

The US, thankfully, has financed itself by selling dollar-denominated debt, pushing currency risks onto its creditors. But so did Iceland. And even Turkey increasingly financed itself in Turkish lira. Particularly in 2005, there were big inflows into Turkey’s local debt and equity markets. Turkey obviously still has a fair amount of dollar debt. It is an emerging market after all. But things were changing.

I still think the financial slump in both Iceland and Turkey could easily turn into a sharp economic slump. In both countries, both policy and market interest rates are up significantly – in part because a weaker currency (and still strong oil) translates into higher prices for imported goods. And I suspect higher interest will, over time, slow the pace of both economies’ expansion.

One big reason why Turkey was growing fast was that because its banks were lending tons of money to Turkey’s households, whether to buy a car or buy a house. But it only makes sense to lend long-term at 13% (say for a mortgage) if inflation and nominal interest rates are expected to fall over time. This year, both inflation and nominal rates rose. Ouch (if you are a bank).

I suspect that the result will be a significant slowdown in credit growth – and in the Turkish economy.

Charles Gottlieb of the European Capital Markets Institute notes that Iceland too was growing in part on the back of a strong expansion of credit (see his figure 1) – though in Iceland’s case, demand for Icelandic Krona was for a while so long strong that Icelandic issuance alone couldn’t meet it. Consequently, European banks started issuing so called Glacier bonds in krona (a note: I am sure the banks hedged their krona exposure, I just don’t know how).

And Gottlieb nicely shows what a sudden stop looks like. See his Figure 4. It shows a huge surge foreign purchases of Icelandic securities issued by Icelandic residents (I think that means it excludes Glacier bonds) up until January of this year. And then a huge – and I mean huge – fall. Inflows became outflows. Foreigners sold; Icelanders bought.

I am not convinced Iceland is the next Thailand – but there are lots of unpleasant outcomes that aren’t quite that severe.

Turkey and Iceland are not the only markets who went through a rather nasty sell-off. Emerging market equities just has their worst run since 1998. Of course, it comes after a huge run-up. And as no shortage of credible observers – like Ragu Rajan of the IMF -- have noted, the markets that are selling off the most are the markets that rose the most. That suggests that the causes of the sell-off are global, a change in the markets willingness to invest in emerging economies, not local – that is what the generally bearish BIS thinks and in this case they have support from some (former?) bulls, like MSDW’s Turkey analyst Serhan Cevik.

Despite this indiscriminate sell-off, there is still no agreement among investors as to what the sudden burst of global volatility actually reflects. …. Risk reduction always brings indiscriminate selling of all ‘risky’ assets at the early stages, regardless of underlying economic structures and policy frameworks.

The team at Danske bank hasn't been as consistently bullish at Cevik, but they seems to agree that it is hard to pin down any fundamental cause of the recent sell-off.

I certainly didn’t see this kind of global sell off of emerging economies coming, though I worried about a few specific markets. And not just ex post. But then again I am usually good for a cautionary quote …

And in some sense, the fact that the current global sell-off focused on emerging economies is a bit strange. I see the logic: what went up too fast has to come down.

But the defining characteristic of the recent boom in private capital flows to emerging economies is that, at least in aggregate, capital was flowing into emerging economies didn’t need the money. The US was attracting more financing that it needed to run very large deficits, and using some of the money to invest in emerging economies. And emerging economies were taking financial flows from say Europe and using them to lend to the US. It was a rather complex equilibrium.

Look at the statistical data in the latest issue of the World Bank’s (very useful) Global Development Finance. Developing economies collectively ran a current account surplus of $245 billion in 2005. Private inflows of $490 billion were used to pay back the IMF and to build up reserves -- these countries reserves were up by $395b or so in dollar terms, more than their current account surplus.

(One note for true balance of payments geeks: the GDF’s reserve increase isn’t adjusted for valuation changes. If you make that adjustment, total reserve growth would be bigger, and the errors and other flows term would fall)

Of course, what happens in aggregate can mask big differences in the specifics. China, Saudi Arabia and Russia all had big current account surpluses. Brazil a more modest surplus. India had a small and growing deficit. Turkey – and Hungary -- had big deficits.

Despite these differences the equity markets of Russia, Brazil and Turkey have all tumbled this year. Foreign funds that poured into these economies earlier this year poured out in May. When the data comes in, the change will look a bit like Gottlieb’s graph showing flows in and out of Iceland.

My hypothesis therefore is twofold:

The recent correction has been driven as much by developments inside the financial markets of the post-industrial economies as by a change in the emerging economies themselves. Hence the general sell-off.

And the impact of the correction will vary dramatically. Some countries didn’t need inflows. Russia. Others did. Turkey. But even in turkey, the inflows that were coming in far exceeded what Turkey needed. In the first quarter, annualized inflows were something like $60b relative to a current account deficit of $30b. If flows go to $30 or $25 Turkey is fine. If they go to zero, not so much.

Actually, my hypothesis is threefold.

In April, the G-7 communique triggered a fall in the market’s willingness to finance US deficits. We saw that in the TIC data. There also was a bit of a surge in capital inflows to Asia that prompted a bout of intervention. Central banks financed the US when markets didn't want to.

In May and early June, folks who borrowed dollars and yen to buy emerging market equities (and debt, to a lesser degree) sold their emerging market equities and repaid their loans. Call it deleveraging.

The net effect has been to help finance the US. Less money was flowing out of the US – US purchases of foreign equities averaged about $10b a month for the first four months of the year. And if Americans may have actually reduced their exposure to emerging economies in May and June. That too would help to finance the US deficit. Deficits can be financed by selling (external) assets as well as issuing (external) debt.

My question: What happens once this process is over?

Do higher US rates continue to draw the financing the US needs to run big current account deficits – a deficit that I still think will be over $900b?

In part because China and the oil exporters continue to use their central banks and oil investment funds to finance the US?

Or does the US join the list of high-carry (at least relative to Japan and Europe) countries that have experienced trouble in 2006?

And what happens if an incipient US slowdown start to generate expectations that US rates have peaked and won’t provide as much support for the dollar?

If I had to guess, I would say Bill Gross (quoted in Business Week) is right.

It's like Peter Pan who shouts, "'Do you believe?' And the crowd shouts back, in unison, 'We believe.'" You can believe in fairy tales and Peter Pan as long as the crowd shouts back, "we believe." That's what the dollar represents, a store of value that people believe in. They can keep on believing, but there comes a point that they don't.Greenspan was here two months ago and talked with us for two hours. The most interesting point was his comment that there will come a time when foreign central banks and foreign investors reach saturation levels with their dollar holdings, and so he sort of drew his hand across his neck as if they've had it. Why can't they keep on swallowing dollars? Logic would suggest that these things start to fray at the fringes. Once the snowball starts it can really get going. ...

The dollar is really well supported by its yield. We've got 5% overnight rates and Japan has zero. You get over 2% relative to the euro, so obviously 5% or 5.25% is dollar-supportive, and the more that Bernanke sounds off that he's going even higher, the more that supports the dollar. The real question is what starts it on the way down? At the moment people believe that's O.K. and yes, housing is starting down, but the rest of the economy is looking good, 2% to 3% GDP growth isn't so bad. I would say that if that's the case we've got a pretty good little fairy tale going here. But if it doesn't, if 5% leads to a crack in the housing market and the unwind of various global markets and the U.S. stock market ... If the stock market keeps going down then that's a sign that 5.25% is too onerous a rate. So what the question becomes then is can the U.S. economy be supported at that level? That's when the question of whether there's the possibility of an avalanche begins. If we get rates then down to 4.5% and then all of a sudden the [other central bankers] are moving up, the money flows out. It's not because of the [lack of a] yield advantage; they've had it up to their necks in terms of dollars. The unwind of the dollar can come from saturation or geopolitical issues or simply that the U.S. economy isn't as strong as people think and they stop believing in Tinkerbelle.

A big fall in the dollar isn’t bad for the US. A big fall in financial inflows that led to a rise in US interest rates though is another story. A 200 bp move is not so big for emerging economies, but it is big for the US. And because the US financial system is much more leveraged, it would also have much bigger consequences.

Basically, to keep other central banks happy when the United States gobbling up debt, Bernanke has to raise interest rates much higher than would normally be warranted, just to avoid a currency collapse. And, he has to do it just when the economy is heading into a recession:

Key gauge points to slowing economy

Index of leading indicators fell more than expected in May as higher gas prices and interest rates start to bite.

June 22, 2006: 4:53 PM EDT

WASHINGTON (Reuters) - A key forecasting gauge for the U.S. economy fell by a larger-than-expected 0.6 percent in May, a report from a private research group showed on Thursday.

The sharp decline in the Index of Leading Economic Indicators from the Conference Board outpaced market expectations for a 0.5 percent fall in May after an unrevised 0.1 percent fall in April.

Ken Goldstein, a labor economist at the Conference Board, cited a slew of factors inhibiting the economy even as leading indicators in European and Asian countries were showing strength.

"The cumulative impact of higher gasoline prices, higher costs to run the air conditioner this spring, a slowing housing market, higher interest rates, a loss of confidence and even higher taxes in some localities, have all combined to slow the forward pace of economic activity, pushing growth to a sub-par level this summer -- possibly extending into the fall," Goldstein said in a statement.

"Given the slower pace, the economy has less ability to absorb another round of strong hurricanes this summer," he added.

Seven of the 10 indicators that make up the leading index fell in May, the Conference Board said.

The largest negative contributor to the index was initial claims for unemployment insurance. The index of consumer expectations made the second largest negative contribution.

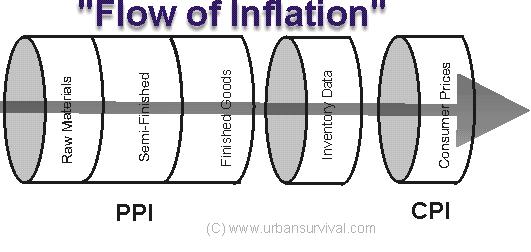

So once again we find ourselves in the paradoxical state of stagflation. High inflation, layoffs and high interest rates. The following piece by James Killus explains why stagflation is not as paradoxical as it seems:

Let me suggest a hypothetical.

Suppose there were two countries, in some sort of neo-colonial relationship. The rich country follows something like the German model, good social benefits, primarily tied to corporate employment, high capital stock, high education levels, and so forth. The poorer country has some social benefits, a social security system, a health care system that is overstressed and that doesn’t cover everybody, stagnating wages, and its capital stock is almost entirely colonial, i.e. the other country owns almost all of it.

Both share a common currency, and on a cash flow basis, the poorer country is sending a lot of cash to the richer country.

Monetary policy from the central bank clearly affects both countries, but both countries can have different fiscal policies. Moreover, cash flows between the two countries can dominate their local monetary policies. The cash flow from the poor country to the rich country has, in fact, produced a liquidity trap in the poor country. By the same token, the same cash flow has created a high degree of liquidity in the rich country, but, because the rich country imports much of its goods and services, it hasn’t seen much CPI inflation. Rather, it has had a series of asset price bubbles.

Now actually I’m talking about a single country here, the United States. The rich country consists of those who have substantial capital assets, and/or are well-situated in the corporate hierarchy. The poor country is low and middle income wage earners without major assets, whose primary asset, in fact, is their share of the social security system, and perhaps a low equity house in a “non-bubble” area like the mid-west.

The major cash flow is the Social Security surplus, which continues to divert enormous sums to the general fund, and the general fund pays out much of its cash to corporate contractors. Also whenever a member of the low income class buys something, a portion of that goes to the rich class, in the form of profits or the wages paid to the affluent class who manage the enterprise.

I think that, with only a few exceptions, “the poor country” has been in a liquidity trap for the past 25 years. CPI price inflation occurs when some of the liquidity that washes over the “rich country” manages to leak into “the poor country.” It is then immediately stamped down by raising interest rates, which pulls yet more money from low income workers (who tend to be debtors). Since high income liquidity primarily affects asset prices, and since asset price inflation is not considered inflation, monetary policy does not react.

Economic “growth” has been confined to the high income group, but since this tends to consist of nominal asset growth, it is not clear to what extent the growth is real. It may be largely an artifact of asset price inflation whose effects have been confined to a part of the economy that doesn’t show up in inflation estimates.

In short, the economy may actually be experiencing stagflation, but that is masked by asset price inflation. Any attempt to turn that nominal growth into actual consumption would trigger CPI inflation, which would immediately be met with interest rate hikes, which further hurt the real economy of low wage earners, but which does little to correct the underlying fiscal malady.

posted by Donald Hunt at 3:31 PM

0 comments

![]()