Signs of the Economic Apocalypse, 6-19-06

Gold closed at 584.70 dollars an ounce on Friday, down 4.8% from $612.50 at the close of the previous week. The dollar closed at 0.7910 euros on Friday, virtually unchanged from 0.7912 for the week. That put the euro at 1.2643 dollars compared to 1.2640 at the end of the week before. Gold in euros would be 462.47 euros an ounce, down 4.8% from 484.57 for the week. Oil closed at 69.97 dollars a barrel Friday, down 2.3% from $71.60 at the close of the previous Friday. Oil in euros would be 55.34 euros a barrel, down 2.4% from 56.65 for the week. The gold/oil ratio closed at 8.36, down 2.3% from 8.55 at the end of the previous week. In U.S. stocks, the Dow closed at 11,014.55, up 1.1% from 10,891.92. The NASDAQ closed at 2,129.95, down 0.2% from 2,135.06. The yield on the ten-year U.S. Treasury note closed at 5.13%, up 16 basis points from 4.97 for the week.

Gold prices continued to plummet last week and U.S. interest rates rose sharply. Everthing else remained pretty much unchanged. If interest rates are rising over fear of inflation and gold is a hedge against inflation, why are gold prices falling? The paradox of gold is that it is both money and commodity. If it is, in effect, a currency, then with inflation the value of gold should go down. Yet, since it is also a commodity, and has been throughout history seen as a safe haven, it’s value should go up in inflationary times. Most likely the price of gold will eventually go up against the paper currencies. What we are seeing is probably both a natural correction as well as an indication of increasing volatility.

Gold, Copper Lead Metals Decline on Concern Over Higher Rates

June 13 (Bloomberg) -- Gold had its biggest plunge in 15 years, falling below $600 an ounce, and copper tumbled to a seven- week low as investors bailed out of commodities and equities on concern about rising global interest rates.

Metals fell for a fourth straight session, the longest slide in three months, and billionaire investor George Soros says the commodity rout isn't over. Federal Reserve Bank of Cleveland President Sandra Pianalto said yesterday inflation exceeded her “comfort level,” boosting prospects for higher U.S. rates. Consumer prices in the U.K. reached a seven-month-high in May.

“The nervousness behind higher rates are anchoring down the markets,” said Michael Guido, director of hedge fund marketing and commodity strategy at Societe Generale in New York. “You have massive global equity losses. Many of these funds are selling secondary and tertiary holdings, which happen to be commodities, to raise cash.”

Gold for August delivery fell $44.50, or 7.3 percent, to $566.80 an ounce on the Comex division of the New York Mercantile Exchange, the biggest percentage drop since Jan. 17, 1991. Prices have tumbled 23 percent from a 26-year high of $732 on May 12. The metal still has gained 31 percent in the past 12 months.

Copper for delivery in three months fell $470, or 6.7 percent, to $6,570 a metric ton on the London Metal Exchange, the lowest close since April 20. The metal is down 25 percent from a record $8,800 on May 11. Prices still have doubled in the past year.

Silver futures for July delivery tumbled $1.44, or 13 percent, to $9.625 an ounce on the Comex. Prices have plunged 37 percent since reaching a 23-year high of $15.20 on May 11.

‘Reduction in Liquidity’

“Commodities probably are in for a period of correction,” Soros told financial news network CNBC yesterday. “We are in a situation where all asset classes are under pressure because of a reduction in liquidity.”

Industrial metals have tumbled from records this year, and gold and silver have slumped in the past month from the highest prices since the early 1980s amid growing speculation higher borrowing costs will stifle the five-year rally in commodities.

U.S. stocks fell for a third day, European equities dropped to a six-month low, and indexes in Japan and Australia had the biggest losses since September 2001. Emerging markets also tumbled.

“There's too much froth in this market,” said David Gornall, head of foreign exchange and bullion at Natexis Commodity Markets Ltd. in London. “People are removing higher risk from their portfolio.”

Gold climbed 18 percent last year and surged 39 percent from the end of 2005 to mid May, partly on demand from investors seeking returns unavailable from stocks, bonds and currencies. Tensions over Iran's nuclear program also boosted the precious metal's appeal as a haven.

‘Hot Money’

“There's hot money in the metals, and it can come and go, lending to volatility both ways,” said A.C. Moore, who manages the $500 million Dunvegan Growth fund in Santa Barbara, California. “People get nervous and sell commodities to raise some cash.”

Shares of mining companies also fell. The Philadelphia Stock Exchange Gold and Silver Index fell 3.92 or 3.1 percent to 120.79. Shares of Freeport-McMoRan Copper & Gold Inc., which operates the largest gold mine in Indonesia, tumbled $2.06 to $44.65.

The European Central Bank raised its benchmark interest rate on June 8 for the third time in six months. South Korea raised its key rate the same day, followed by India and South Africa. At least four Fed officials said last week they're concerned about inflation.

Interest-rate futures show traders are pricing in a 90 percent chance the Fed will raise its benchmark rate a quarter-percentage point to 5.25 percent at its meeting late this month, up from 84 percent odds yesterday and 72 percent on May 31.

U.K. Rates

U.K. consumer prices rose 2.2 percent from a year earlier after rising 2 percent in April, the Office for National Statistics said today, making it more likely the Bank of England will raise rates. Prices paid to U.S. producers in May also rose more than forecast, stoking inflation concerns.

“The fears of a slowing economy are going to cast doubt on the demand for metals,” said James Vail, who manages $700 million in natural-resource stocks at ING Investments LLC in New York. “It's a very unsettling time. We're overreacting on the downside as much as we were overreacting on the upside.”

The rising cost of gasoline propelled U.S. consumer prices higher last month, giving Federal Reserve policy makers reason to fret they're losing their grip on inflation, economists expect a report to show tomorrow.

‘Play Defense’

The consumer-price index rose 0.4 percent in May after a 0.9 percent gain the prior month, according to the median forecast of 72 economists surveyed by Bloomberg News.

Metal prices will tumble should the index increase more than forecast, some analysts said.

“The CPI is more Main Street,” Guido of Societe Generale said. “A higher number and the metals market continues to play defense.”

Demand still outstrips supply and the rally in metals may resume, Vail at ING said. Speculators increased copper purchases earlier this year amid forecasts global production will lag behind consumption.

“It's very difficult in today's world to find new supplies, and companies are having difficulty in meeting production targets,” Freeport-McMoRan Chief Executive Officer Richard Adkerson said today in an interview. Output will be lower in 2006, and “even at today's prices, we have the opportunity to have even a stronger year,” he said.

Time to Buy?

Some investors say the price decline offers a buying opportunity for some metals.

HSBC Holdings Plc estimated last month about $100 billion will be invested in commodity indexes by the end of 2006, compared with $10 billion at the end of 2003.

“This is not the end of the commodities rally,” said Michael Widmer, an analyst at Macquarie Bank Ltd. in London. “The fundamentals for most commodities, such as gold, are strong.”

Moore of Dunvegan, who sold some shares of the StreetTracks Gold Trust exchange-traded fund as the metal was rising to a 26- year high, said he's considering buying metals.

“We're more interested in gold and metals generally,” Moore said. “There's still a bull run in gold, and the money will be back.”

The drop in gold prices has emboldened those who have always ridiculed “gold bugs.” Al Martin does his share of ridiculing in the following piece, but ends up recommending that many people should buy and hold gold, primarily because he sees a collapse in the value of the dollar within three years:

For investors, the question of whether to buy precious metals is tied up with the likelihood of inflation or deflation. If there is deflation, cash is a good investment, if there is inflation gold and other commodities become more attractive. Analysts seem to be divided on the inflation versus deflation debate. But, as the following column in Forbes indicates, that very uncertainty should ultimately strengthen gold:What is [gold’s] ultimate value? Its ultimate value is as an inflation hedge, not as an alternative investment, not maintenance of purchasing power in a would-be deflationary environment. Its ultimate and final value is money. It is the currency of last resort. That is its final and ultimate value. And that is the value that the stuff has to the gold bugs.

…The financial apocalypse that people believe are waiting for will come about when the U.S. dollar falls apart. Why? Because the U.S. dollar is the ultimate currency. In the realm of paper currencies, the U.S. dollar is the ultimate currency. When the U.S. dollar falls apart, that’s when everything else falls apart.

…Thanks to Bushonomics I (Bush Sr.) and II (Bush Jr.) as well as the enormous multi-trillion-dollar accrual of debt that occurred from 1981 to 1992 and again from 2001 to present, the multi-trillion-dollar accrual of debt reduces the United States’ future financial flexibility by increasing future liabilities -- both real and contingent because of this debt and the strangulation that debt has.Debt has what’s called a re-strangulation effect over time. Even though the value of the currency may be debased by purposeful action of the government in an effort to monetize existing debt, you can’t monetize debt endlessly, which is what the United States is close to having to do.

David Walker, the Comptroller General of the United States, pointed out that, should the Bush Cheney Regime be re-ensconced in power for a second term and the fiscally corrosive practice of Bushonomic, i.e., negative debt finance consumption, be continued, then the United States would not be able to service its debt past 2009. That’s when the game ends. That’s when it all falls apart. When the United States government can no longer service its debt, the currency becomes worthless, or very nearly so.

…Unless the United States can engineer (the Bush Cheney Regime through economic policy and the Fed through market action) a dramatic fall, which would be at least another 40%, the ensuing decline in the dollar would help to monetize debt.

As we have explained debt monetization before, it is nothing more than the issuance of debt and the future servicing of the debt in ever-cheaper currency, which obviously causes interest rates to rise, which causes inflation and is something that this regime is desperate to create.

Despite having a Federal Reserve that has maintained money supply targets, in some cases, twice above what they would normally be maintained relative to GDP, they simply haven’t been successful in creating inflation in the United States because of the latent deflationary pressures that Bushonomics causes.How do you create deflation? Through the accrual of debt within all 3 legs of what could be called the national stool, i.e., government, business and industry, and the people.

We are now in a situation where government debt is at all levels of government–federal, state, local a record high. We also have a situation where consumer debt is also at an all-time high -- not only in the United States, but almost in every other country at the same time. Thus there are global deflationary pressures. How do you combat this deflation? You have to create some inflation.

This is simply the cheapening of money in order to repay existing debt in the future and make that less of a burden relative to total income, which is not only something that affects governments, but it affects business and industry, and the people as well.

The problem with Bushonomics, however, is that it adds in a new factor, namely, that the people aren’t able to successfully monetize debt the way government does. Under Bushonian Regimes, real wages, i.e., wages not including inflation, actually fall.

The reason they do so is because, under Bushonian Regimes, economic policies to dramatically increase the rate of productivity and to consequently decrease per-unit labor cost, are pushed.

Look at the tremendous increase in the rate of productivity that has occurred under the Bush Cheney regime.

…The answer is a conundrum. Gold is good. Gold is what you want to own. If you’re not a trader, or if you don’t have the smarts to trade it, …you still want to hold gold. Gold is the asset you want to hold.But why do you want to hold it? Therein becomes the question that separates the gold bugs from the gold bulls. Why do you want to hold it? Do you want to hold it as an investor with the idea of selling it at some point in the future to take a profit?

That’s not the reason why the average citizen should be holding gold, because they’re not smart enough to time the markets in order to take a profit, simply put, to sell it high and buy it low, as they say. The reason why the average citizen should be holding gold is because of gold’s ultimate capacity as the money of last resort, knowing that it is now likely that the United States will not be able to service its debt after 2009.

Or that in order to continue to do so, it would have to create a hyper-inflationary scenario, which would only postpone the inevitable for a few years -- 4 years, or 6 or 8 years, maybe, at the most.

Ultimately, hyper-inflationary bubbles cannot be sustained. They burst and everything falls apart. Witness the 1981 “Bolivian Meltdown” wherein the Bolivian peso fell to a value that the physical weight of the banknotes was equal to the price of tomatoes.

Here is another analyst bullish on gold:James Grant

06.19.06, 12:00 AM ET

Gold is an August monetary asset but an undependable investment. Producing no income, it is inherently speculative. I am a value investor, but I am also a gold bull. I ought to try to explain myself.

Value investors buy stocks or bonds by the numbers. They compare price with value and buy if the discount is suitably deep. They turn a deaf ear to macroeconomic theorizing. Whether the gross domestic product is rising briskly or not at all is immaterial if a particular company is priced at less than its readily ascertainable net asset value.

Gold is something different. You buy it solely for macroeconomic considerations. I buy gold as a hedge against the stewards of paper money. I buy Krugerrands, the metal itself, suitable for burying in the turnip patch. I expect the price of the South African gold coins to keep going up, but I don't know how high.

There is much I don't know about gold. There is much that nobody can know--critically, for example, what the price ought to be. It's guesswork. If this is a cockamamie way to invest, I draw courage from the theory of central banking, which is more cockamamie still. These days it boils down to picking an interest rate and imposing that rate on the market. Some would call this "price-fixing." Can you name a single successful government price-fixing operation?

For a year, through June 2004, the Federal Reserve held the federal funds rate at 1%. Chairman Alan Greenspan and the chairman-to-be, Ben S. Bernanke, said they were fighting an anticipatory battle against deflation. They wanted to preserve the U.S. from a Japanese-style funk following the bursting of the stock-market bubble in 2000--01. So they dropped lending rates to the floor and pushed home prices to the moon.

Now house prices are falling, and mortgage rates are rising, which brings to mind Greenspan's advice to U.S. homeowners in February 2004.

He suggested they take out adjustable-rate mortgages. Many did--and are discovering that their disposable income, after mortgage payments, is adjusting to the down side. The real-estate-dependent U.S. economy is starting to wheeze.

And inflation is inconveniently starting to percolate. It's a quirk of the U.S. statistical apparatus that residential rents count for 29% of the measured rate of consumer price inflation. During the housing-price boom, rental rates sagged. But now that homeownership is losing some of its luster, rental rates are turning up. They are taking the Consumer Price Index up with them.

You are Chairman Bernanke. What do you do? A conscientious fellow, you try first to do no harm. You have made a lifelong study of deflation and the Great Depression. Of all the mistakes you could make at the helm of the Federal Open Market Committee, there is one you really want to avoid: You do not want to go down in history as the scholar of the Great Depression who inadvertently steered the highly leveraged U.S. economy into Great Depression Part II. You will be slow to tighten monetary policy when home prices are deflating, let the CPI be what it may.

Gold competes with the Bernanke dollar, just as it did with the Greenspan dollar and just as it has with government-issued money since the invention of the printing press. The historical record is undebatable: 1) Currencies ultimately lose their value. 2) Gold is a lousy long-term investment. 3) Yet when markets lose confidence in paper, there is nothing quite like a Krugerrand.

How confident are you? The U.S. annually consumes much more than it produces. It finances the deficit with dollars. More than $1.6 trillion has come to rest on the balance sheets of foreign central banks (as opposed, say, to the bank accounts of profit-seeking corporations). In recent months some of these central banks have signaled their intention to diversify into other currencies. Some of them have indicated they are buying gold.

The post-1971 dollar is uncollateralized. Its value is derived from the world's faith in America as much as from the strength of the U.S. economy or the level of U.S. interest rates. Reading the newspapers, I judge that faith to be wavering.

The gold price has doubled in the past three years. But it has only just kept up with the price of lead and has badly trailed the prices of copper and zinc.

Arguably, then, gold's rise to date is not as much a reflection on U.S. monetary management as it is an echo of the commodity boom.

You can be sure that gold will have its own bull market when the dollar resumes its bear market.

When will that day come, and how high is up? I don't know--and neither does Bernanke.

James Grant is the editor of Grant's Interest Rate Observer. Visit his homepage at www.forbes.com/grant.

Bernanke Scares Pavlov's SheepOn the deflationary side, housing inventories are rising, indicating sharp drops in prices soon:

Richard Benson

June 13, 2006

Ivan Petrovich Pavlov was a brilliant Russian Physiologist whose experiments on animals led to discoveries that would make the demented doctors in World War II, in both Germany and Japan, very jealous. Some of Pavlov’s early work was done on sheep. Unfortunately for the sheep, the experiments on them were so stressful they eventually died of heart attacks. Pavlov’s work on sheep, analogous to stock market investing, is critical for this article because speculators, hedge funds, and particularly retail stock investors, do tend to act a lot like sheep.

Pavlov’s work on the conditioned reflex reaction of sheep to stimuli should be of the utmost importance to the Federal Reserve and world central banks at this juncture in a world where signs of speculative excess – even to the bubble level – clearly remain in all major risk asset classes including housing, commodities, emerging markets, and even major stock markets.

In Pavlov’s research, he discovered that if he gave the sheep a mild electric shock, it would bother them very little and their life would go on pretty much as if nothing had happened as long as the shocks were random. Warning the sheep in advance of a shock by ringing a bell, however, affected their behavior and it changed radically. The sheep were just smart enough to realize that if they heard the bell, the shock was coming. After repeating this exercise a few times, the poor sheep lost control of bodily functions and after a few more warning bells, they started dying of heart attacks.

What Ben Bernanke and the Federal Reserve Governors should know, and are likely to find out the hard way, is that markets driven by speculation will react just like Pavlov’s sheep. Indeed, the major market participants and speculators, particularly greedy retail investors, are there to get “sheared at market tops”. Somebody has to buy when the smart money wants to sell and take their winnings out of the casino. Moreover, to keep the herd of retail investing sheep grazing on financial investments including commodities, there needs to be a steady stream of “feel good” press for stocks about how great productivity is and how the nomination of the new Treasury Secretary, Hank Paulson, will be good for the dollar. All the while, stock analysts and market touts are claiming “there has never been a better time to invest”.

With fears about a rising core inflation rate and slowing economic growth, Bernanke and the Federal Reserve Governors understand too much money was printed up over the last decade. They’re not alone. The central banks in Europe are not done raising interest rates either and Japan is just beginning to raise their rates from zero to drain excess liquidity. After 16 rates hikes, the Fed announced it is not done raising rates. This “ringing of the bell” has the sheep sensing that more shocks are coming. This could be downright ugly for the financial markets! We would recommend that the Fed have plenty of tranquilizers and lots of liquidity available to bail out the markets if they keep on scaring the sheep.

The market participants that started running like lemmings for the edge of the cliff are led by the market professionals! They have been heard shouting “get out before the sheep panic!” Over the last few months, easy money trades are down, and some Middle Eastern markets have crashed while other emerging markets are in a bear market. Commodities are also in a serious correction, including gold and silver.

All too often central banks tighten until the financial markets suffer a significant failure. The Federal Reserve and Treasury have regular practice “fire drills” on what to do during a market crash, and given their behavior and what Pavlov taught us about sheep, they will more than likely create an opportunity to fight a real financial market fire. However, when the Fed has to fight a market event – and cuts interest rates in an effort to save the lives of some of the sheep – you can kiss the dollar goodbye. So, while the dollar has gotten a technical lift over the past week or so, my cash is still going into “non-dollar cash”. The U.S. trade deficit is so massive, and our debt is so large, we believe the dollar will have to fall much lower.

While a general stock market crash may pressure all stocks (including precious metal stocks) to go lower, precious metals and precious metal stocks are being offered now at significant discounts (much of the excess that causes sharp drops in price has been washed out).

In the years ahead, the high prices we have all seen in gold and silver will be surpassed many times over. In addition, leaving your money in short-term cash with no price risk while receiving 5 percent, looks a lot better than losing money in stocks or real estate! Suddenly, risk is a four letter word and cash is not trash.

The Producer Price Index numbers for May were released last week, raising inflation concerns:Cheerleader Panic, the HPI, and the Battle of New Orleans

Michael Shedlock

Saturday, June 10, 2006

Speaking for the National Association of Realtors on June 6th, David Lereah, the NAR’s top cheerleader had this to say:

Home sales are settling into a slower pace. “In recent years we were occasionally challenged to find appropriate superlatives to describe surprisingly high home sales,” he said. “Now the housing market has cooled, but 2006 is still expected to be the third strongest on record. In this case, experiencing a slowing from a hot market is a good thing because we need a solid housing sector to provide an underlying base to the economy, and slower appreciation will help to preserve long-term affordability. But this is a time for the Fed to pause on rate hikes because we have some interest-sensitive housing markets that have become vulnerable.”

Let's summarize:

This year will be the "third strongest on record".

Slowing from a hot market is a "good thing"

"Slower Appreciation will preserve affordability"

"The Fed should Pause"

It's now Mish Question Time (but this is an easy one).Which one of the above does not logically fit in?

Ding Ding Ding the answer of course is number 4.

Lereah is now in panic mode,talking out of both sides of his mouth at the same time. I am not the only one that noticed this either.

In "Burning Down the House" Independent economist Bob Brusca had this to say:

The 10-year note is still yielding just 5%, and 30-year mortgage rates are still historically reasonable. In that light, Mr. Lereah's demand "smacks of desperation," and might cause enough alarm to make potential first-time home-buyers more likely to stay on the sidelines. "I would see this as a mistake [on Mr. Lereah's part] and not an indicator of bad things to happen," Mr. Brusca said, adding: "Except for home builders."

... What is David Lereah really worried about?

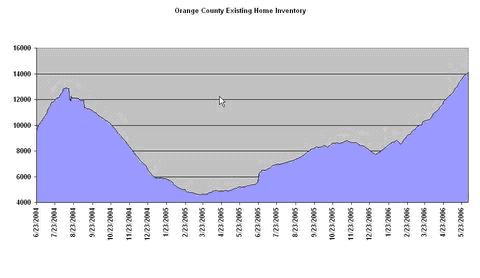

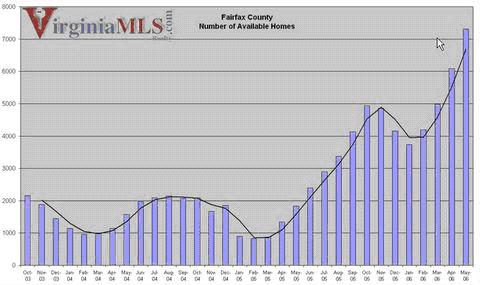

…Lereah knows things are rapidly deteriorating or he would not be so contradictory. But the three things that probably worrying him most are inventory, inventory, and inventory. The next four things he is worried about are falling sales, falling prices, rising foreclosures, and rising bankruptcies. Let's take a quick look at some recent inventory charts.

Orange County

Fairfax County VirginiaThere is little atypical about any of the above charts.

Florida looks the same way and I am sure countless other places do too.

Beneath the facade I sense David Lereah is in a near panic.

How long he can remain an optimistic cheerleader rooting for a team down 20 points in the fourth quarter with under 2 minutes left remains to be seen. I am already ready for the next ploy: "Homes won't stay at these prices forever". He will of course be correct. Prices will head lower, much lower. We have only just begun to unwind the craziness of the last few years.

Producer prices up more than expected

By Mark Felsenthal

U.S. producer prices excluding energy and food rose faster than expected last month and high gasoline prices boosted otherwise tepid retail sales, the government said on Tuesday in reports that signal inflationary pressures.

U.S. producer prices rose just 0.2 percent last month as food costs fell, but prices outside of food and energy rose a steeper-than-expected 0.3 percent. Retail sales in May rose just 0.1 percent, matching Wall Street expectations, with declines in auto, furniture and building material sales.

Analysts said the rise in core producer prices shows the risk that rising prices may be working their way from producers to consumers.

"Pipeline inflation pressures continue to build, and that impression was not dispelled by today's release," said William O'Donnell, head of U.S. interest rate strategy and research at UBS in Stamford, Connecticut.

The dollar climbed to its highest levels in over a month against the euro and the yen as the higher-than-expected core producer price reading heightened expectations the Federal Reserve would raise interest rates in June.

U.S. Treasury debt prices pared gains, while stocks were little changed in volatile trading.

The producer price report "supports the idea that (the Federal Reserve) will raise rates another 25 basis points on June 29, and the dollar has reacted positively to that," said Alex Beuzelin, foreign exchange market analyst at Ruesch International in Washington.

The consumer price report for May will be released on Wednesday, providing a much broader outlook on inflationary pressures. Analysts expect the 0.4 percent rise in the CPI, while the core rate is expected to rise on 0.2 percent.

George Ure points out that crude goods rose in May by a 2% monthly rate which means a 26.8% annual rate.

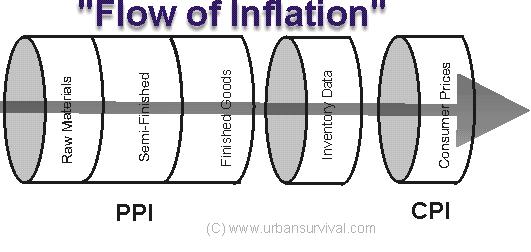

Looking ahead, it’s hard to see whether the ultimate fear should be inflation or deflation. Doug Casey says both can happen at the same time:PPI: Crude Goods: 26.8% Inflation

Welcome to the Weimar? It depends on how much of the coming increases in crude goods are passed on to consumers, but here's the picture: Crude goods are up - a lot! 2% from last month to this (May) report and that pencils out to an annual rate (26.8%) that could spell disaster for the markets, especially in light of inflation results from elsewhere which we'll get to in a minute.

To keep things in perspective, here's how the flow of inflation data looks like when you step back far enough from the numbers:

So what we're talking about today is inflation down the supply chain a ways from where it hits the retail outlets where the numbers morph into CPI (consumer prices) which will come out tomorrow.

Now, here's where things are by the Labor Department's latest:

"The Producer Price Index for Finished Goods rose 0.2 percent in May, seasonally adjusted, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. This increase followed a 0.9-percent jump in April and a 0.5-percent advance in March. At the earlier stages of processing, prices received by manufacturers of intermediate goods climbed 1.1 percent in May after rising 0.9 percent in the preceding month, while the crude goods index moved up 2.0 percent following a 1.2-percent gain in April. "

Now this is absolutely key: At the Crude Goods level (Raw Materials) prices are going up like crazy. Why? Haven't you been paying attention to our "inflation is a worry" discussions?

The change in crude goods of 2% for the month - which is the same as saying 26.8% inflation is working its way into the front end of the pipeline.

The report makes it sound like the slight improvement in finished goods is just a twitch of energy price impacts:

"Most of the deceleration in the finished goods index can be traced to prices for energy goods, which slowed to a 0.4-percent increase in May after advancing 4.0 percent in April. Prices for finished consumer foods turned down 0.5 percent following a 0.1-percent gain in the prior month. Alternatively, the index for finished goods other than foods and energy increased 0.3 percent in May compared with a 0.1-percent rise in April."

"Before seasonal adjustment, the Producer Price Index for Finished Goods advanced 0.4 percent in May to 161.2 (1982 = 100). From May 2005 to May 2006, prices for finished goods increased 4.5 percent. Over the same period, the index for finished energy goods climbed 20.6 percent, prices for finished goods other than foods and energy rose 1.5 percent, and the index for finished consumer foods fell 1.5 percent. For the 12 months ended May 2006, prices for intermediate goods increased 8.9 percent and the crude goods index moved up 8.6 percent."

OK, there you have it: The BLS folks admitting that there is 8-9% inflation down the pipeline.

The Greater Depression—an Update

Doug Casey

June 5, 2006

…[A] depression is probably inevitable this time.The only serious question in my mind is whether it will be essentially deflationary in nature, as it was the case in the U.S. in the 1930s, or inflationary like in Germany in the 1920s. My guess is the latter because the government is so much more powerful today. Or it could actually be both at once, in different sectors of the economy.

How?

Inflation could drive interest rates to 20%. This would collapse the bond and real estate markets, wiping out trillions of dollars of purchasing power—which is deflationary. Meanwhile, that same inflation doubles the cost of food and fuel. In other words, the opposite of what we’ve mostly had for the last generation, when we had “good” inflation in stocks, bonds and property, but stable or dropping prices in “cost of living” items. This time the pattern could reverse, which would be a nightmare for most people.

And as people become more focused on speculation in a generally futile attempt to stay ahead of financial chaos, they inevitably divert effort from economic production. Which will decrease the general standard of living even more.The situation isn’t made easier by the possibility that we’re facing Peak Oil—the start of a secular decline in world oil production. Or the fact that Americans, both individually and collectively, are deeply in debt and living on the kindness of strangers. The problem with debt is that it artificially increases our standard of living. But when we pay it off, especially with interest, it reduces our standard of living in a very real way.

Wrap this economic environment around the so-called War on Terror, which is rapidly morphing into the War on Islam, which could easily turn into World War III, and you’re looking at the perfect storm. The odds of a major conflagration are very high, and it’s not being adequately discounted. If Bush starts a war against Iran, or if another incident like that of 9/11 occurs, or even if the trend of the last five years accelerates, the U.S. is going to be locked down like one of its numerous new federal penitentiaries. And that will be accompanied, and compounded, by mass hysteria among Boobus americanus.

At that point, your investment portfolio will be among your lesser concerns. People forget that, in every country and time, there’s a standard distribution of sociopaths and misdirected losers. In normal times, they seem like normal people. But when the time is right, they show their colors, and they love to get jobs with the government, where they can lord it over their betters.

Is the Greater Depression really inevitable? How bad will it be? Is there another side to the argument? Can it be avoided?

I suppose it’s not absolutely inevitable. Perhaps friendly aliens will land on the roof of the White House and present the government with a magic technology that can undo all the damage it’s done. But we live in a world of cause and effect where actions have consequences. That being the case, I expect truly serious financial and economic trouble…

posted by Donald Hunt at 1:58 PM

![]()

0 Comments:

Post a Comment

<< Home